Exponentially Weighted Moving Average

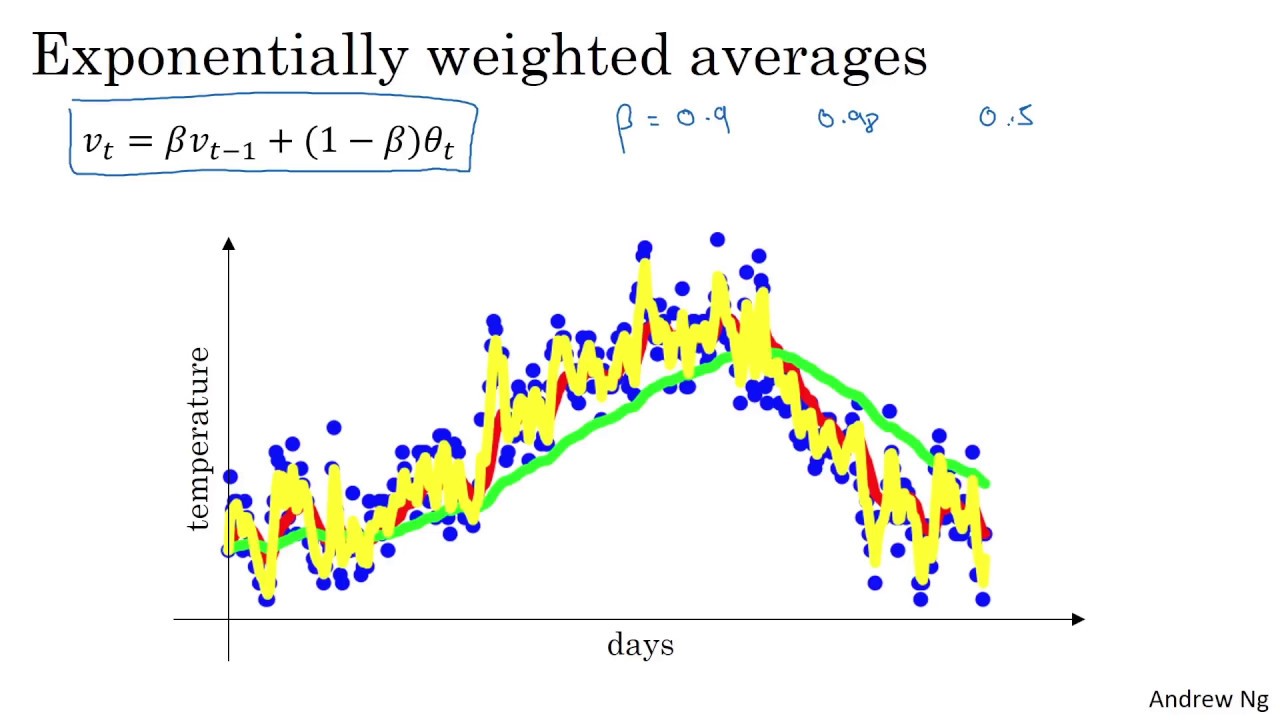

Vt* = *β* * *Vt − 1 + (1 − β)θt*; *θt − currentdatapoin**t

We usually average of $\frac{1}{1-\beta}$ datapoints; for β = 0.9 we average over 10 datapoints

Vt* = *β* * *Vt − 1 + (1 − β)θt*; *θt − currentdatapoin**t

We usually average of $\frac{1}{1-\beta}$ datapoints; for β = 0.9 we average over 10 datapoints